Municipals were little changed Thursday as inflows to municipal bond mutual funds returned. U.S. Treasuries were weaker five years and out, and equities ended up.

The two-year muni-to-Treasury ratio Thursday was at 58%, the three-year at 59%, the five-year at 59%, the 10-year at 59% and the 30-year at 86%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 59%, the three-year at 58%, the five-year at 58%, the 10-year at 60% and the 30-year at 87% at 4 p.m.

Lighter trade volumes have begun ahead of the holiday-shortened final week of 2023 while slim new-issue volume kept market activity limited.

“The market has been grinding higher as people seem to have cash, and have the heavily positive January technical in mind,” Greg Shuman, portfolio manager at Lord Abbett, said Thursday.

“Tax-loss harvesting has been slowing down given the market rally that has occurred over the last six weeks,” Shuman added.

While munis were little changed Thursday, and UST yields rose five years and out, muni yields have been shifting lower along with USTs over the past month or so, said Jeff Timlin, a managing partner at Sage Advisory.

“Changing investor expectations regarding Fed policy shifts and timing has led to persistent and volatile yield moves,” he said.

Like the Treasury curve, he noted muni yields “continue to be inverted in the front-end with significant slope in the back-end.”

An inverted yield curve, though, “will not last for long as they are indicative of an economic slowdown to come,” he said.

Muni yields could even fall further, he said.

The 10-year AAA muni yield topped 3.50% in 2023. Since Nov. 1, the 10-year spot has fallen 130 basis points, according to Refinitiv MMD data.

“Although inflationary pressures persist, tight credit conditions are slowing economic activity,” Timlin said. “If the economic slowdown persists, yields are projected to go lower, especially front-end rates.”

Seasonal factors have contributed to a favorable return environment, he said.

“December and January represent a period of heightened demand and limited supply,” Timlin said.

Bond Buyer 30-day visible supply sits at $3.56 billion.

Demand remains high, he noted, “as over $50 billion in maturity and coupon payments come due from Dec. 1 to Jan. 15.”

New-issue supply comes to a “virtual halt” as muni issuers stop coming to market between Dec. 15 and Jan. 15.

There are also rare technical factors that have indicated an above-average return environment, he noted.

“Historically, when mutual fund flows turn negative and excessive negative returns ensue, positive returns follow,” Timlin said.

This valuation gap “presented itself in November, a historic month for munis,” he said.

The broad Bloomberg municipal index returned 6.35% for November, the highest returns in three decades.

The high-yield index returned 7.75%, and taxables posted returns of 4.95%. After November’s gains, year-to-date, munis are returning 6.16%, high-yield 9.23% and taxables 8.57%.

While outflow cycles can be “painful,” Timlin noted, “they have been temporary and offer excellent entry points.”

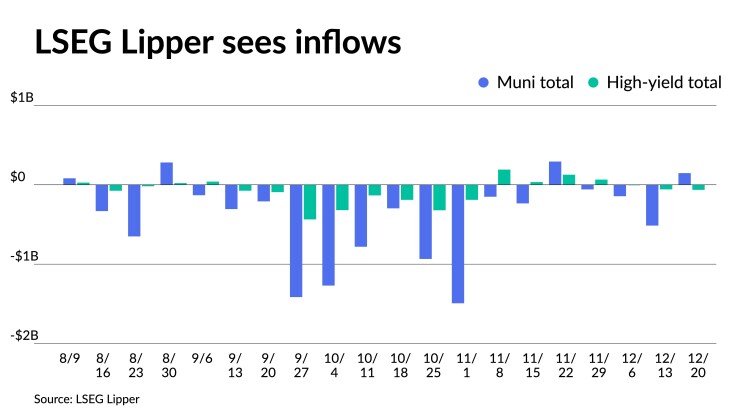

The end of the outflow cycle could be near. LSEG Lipper reported Thursday that investors added $147 million to muni mutual funds for the week ending Wednesday after outflows of $514.5 million the week prior.

High-yield saw outflows of $64.2 million after outflows of $58.5 million the week prior.

Other market participants said the year is ending on a much more positive note than it began.

There is an upbeat tone to end the year following the November rally, according to Tom Kozlik, managing director and head of public policy at HilltopSecurities.

“Market expectations are a little more balanced to optimistic because most believe the Fed is through, and easing is likely to take shape in 2024 sometime,” Kozlik added.

Secondary trading

NYC 5s of 2024 at 3.29%-3.04%. California 5s of 2025 at 2.62% versus 2.64% Wednesday. New Mexico 5s of 2026 at 2.55%-2.50%.

Dallas County, Texas, 5s of 2027 at 2.45% versus 2.53% Friday. Maryland 5s of 2028 at 2.30% versus 2.34% Wednesday. DASNY 5s of2032 at 2.40%-2.34% versus 2.43%-2.48% on 12/14.

NYC TFA 5s of 2040 at 3.04% versus 3.43% on 12/12 and 3.48%-3.47% on 12/11. DASNY 5s of 2041 at 3.14% versus 3.16% Wednesday. LA DWP 5s of 2042 at 3.09%-3.08% versus 3.38% original on 12/8.

Garland ISD, Texas, 5s of 2048 at 3.57%-3.56% versus 3.56% Wednesday and 3.68%-2.67% Monday. NY State Urban Development Corp. 5s of 2056 at 3.81% versus 3.81% Friday.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.69% and 2.54% in two years. The five-year was at 2.28%, the 10-year at 2.28% and the 30-year at 3.47% at 3 p.m.

The ICE AAA yield curve was little changed: 2.74% (unch) in 2024 and 2.55% (unch) in 2025. The five-year was at 2.27% (unch), the 10-year was at 2.31% (unch) and the 30-year was at 3.46% (-1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.68% in 2024 and 2.55% in 2025. The five-year was at 2.31%, the 10-year was at 2.34% and the 30-year yield was at 3.43%, according to a 3 p.m. read.

Bloomberg BVAL was bumped up to a basis point: 2.58% (unch) in 2024 and 2.49% (-1) in 2025. The five-year at 2.21% (unch), the 10-year at 2.27% (-1) and the 30-year at 3.36% (-1) at 4 p.m.

Treasuries were weaker five years and out.

The two-year UST was yielding 4.348% (-2), the three-year was at 4.059% (-2), the five-year at 3.878% (+1), the 10-year at 3.887% (+2), the 20-year at 4.198% (+3) and the 30-year Treasury was yielding 4.027% (+3) near the close.