Municipals were steady Friday, ignoring weakness in the U.S. Treasury market after the jobs report came in hotter-than-expected. Equities ended up.

The November payroll report “was stronger than Wall Street was expecting, and we are already seeing significant upward pressure on Treasury yields,” said Scott Anderson, chief U.S. economist and managing director at BMO Economics.

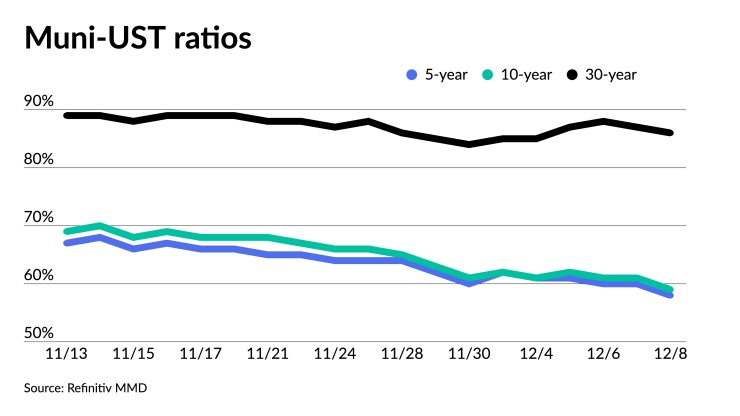

Muni yields were little changed while UST yields saw the greatest losses on the short end.

“Today’s payrolls and market reaction in the aftermath of the release with UST yields moving higher is a possible indication of things to come,” according to Barclays PLC.

Moving forward, “the current rally will likely take a pause very soon, especially in Treasuries, though how the muni market may respond is open given the strong seasonality for munis from December 2023 to February 2024,” BofA Global Research strategists said.

And after such a strong performance in November, Barclays strategists Mikhail Foux, Clare Pickering and Mayur Patel believe “there is very little juice left from both an absolute and relative point of view.”

UST yields are expected to be “meaningfully higher” next year, especially during the first quarter, and at current ratios and spreads, “there is little cushion to absorb a possible large move higher in rates,” they said.

The two-year muni-to-Treasury ratio Friday was at 58%, the three-year at 58%, the five-year at 58%, the 10-year at 59% and the 30-year at 86%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 60%, the three-year at 59%, the five-year at 59%, the 10-year at 62% and the 30-year at 86% at 4 p.m.

The 10-year muni-UST ratios are four to five percentage points higher than 2021’s all-time lows, they said.

The five- and 30-year ratios “have more juice, but the average and the median for these data series going back to 2018 are still substantially higher compared with current levels, even if we remove the extremes of 2020 from consideration,” Barclays strategists said.

In recent history, there were only a few times when tax-exempts lost money in December, “as it is normally a very strong month for the asset class, while supply is typically not overwhelming,” they said.

Moreover, Barclays strategists said mutual funds will get a “sizable inflow” in January from coupons and redemptions.

Therefore, they are not worried about muni performance this month.

They are “still a bit cautious looking ahead to 2024,” despite the supportive nature of market technicals at the moment.

December through February 2024 should be a period with a strong supply/demand imbalance, BofA strategists said.

“Under such favorable conditions, if Treasury yields rise significantly, muni yields will likely follow quite slowly, they noted.

New-issue calendar

The new-issue muni calendar is estimated at $3.329 billion next week with $1.927 billion of negotiated deals on tap and $1.401 billion on the competitive calendar, according to Ipreo and The Bond Buyer.

The City of Virginia Beach Development Authority leads the negotiated calendar with $463 million of residential care facility revenue bonds, followed by Ohio with $383 million of GOs.

The competitive calendar is led by $847 million of state personal income tax revenue bonds from the Empire State Development in three deals.

Secondary trading

Georgia 5s of 2024 at 2.77%. LA USD 5s of 2024 at 2.81%. Maryland 5s of 2025 at 2.76% versus 2.85% on 11/29 and 3.07% on 11/21.

California 5s of 2027 at 2.53%. DC 5s of 2028 at 2.53%. Minnesota 5s of 2028 at 2.46%.

Bay Area Toll Authority, California, 5s of 2031 at 2.39%. NYC TFA 5s of 2032 at 2.75%. Chandler, Arizona, 5s of 2035 at 2.61%-2.62% versus 2.66% Thursday and 2.73%-2.74% original on Tuesday.

Massachusetts 5s of 2053 at 4.11%-4.07% versus 4.06%-4.05% Thursday and 3.99%-3.80% on 12/1. Hillsborough, Florida, 5s of 2053 at 3.91% versus 4.07%-4.06% on 11/29.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.92% and 2.72% in two years. The five-year was at 2.47%, the 10-year at 2.50% and the 30-year at 3.71% at 3 p.m.

The ICE AAA yield curve was little changed: 2.90% (unch) in 2024 and 2.73% (unch) in 2025. The five-year was at 2.46% (-1), the 10-year was at 2.56% (unch) and the 30-year was at 3.68% (+1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.88% in 2024 and 2.75% in 2025. The five-year was at 2.54%, the 10-year was at 2.63% and the 30-year yield was at 3.65%, according to a 3 p.m. read.

Bloomberg BVAL was cut up to one basis point: 2.79% (unch) in 2024 and 2.71% (unch) in 2025. The five-year at 2.44% (unch), the 10-year at 2.53% (+1) and the 30-year at 3.60% (+1) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4722% (+14), the three-year was at 4.459% (+13), the five-year at 4.247% (+13), the 10-year at 4.236% (+10), the 20-year at 4.494% (+7) and the 30-year Treasury was yielding 4.313% (+7) near the close.

November jobs report comes in higher than expected

Job growth in November came in above consensus expectations, with 199,000 jobs being added, said Wells Fargo Securities senior economists Sarah House and Michael Pugliese

“U.S. labor market conditions remain tight,” said Brian Coulton, chief economist at Fitch Ratings.

“Payrolls growth of over 200,000 a month on average in the last three months is well above the long-run sustainable rate of job expansion and it looks as if the participation rate has hit something of a plateau, limiting the growth in labor supply,” he said.

With the unemployment rate declining to 3.7% and average hourly earnings growth picking up to 0.4% month-on-month, “this will fuel concerns at the Fed that nominal wage inflation will get stuck at current levels, which are too high from an inflation target perspective,” Coulton said.

“Today’s payrolls print signals that labor markets continue to generate healthy job growth, and the dip in the unemployment rate is showcasing that labor markets are making incremental progress without experiencing material damage from inflation improvement,” said Candice Tse, global head of strategic advisory solutions at Goldman Sachs Asset Management.

Regardless of the favorable monthly readings in November, House and Pugliese said “the labor market clearly has cooled over the course of the year.”

Employment growth “continues to come down from its post-pandemic boom, wage growth is slowing and labor turnover has receded as greener pastures at a new employer are not quite as enticing as they were earlier in the expansion,” they said.

Beneath the headline figures, House and Pugliese said “there are signs that the margins of the labor market are deteriorating, with job gains being more narrowly driven, temporary help employment declining and laid off workers taking longer to find new employment.”

“This report is showing a labor market that continues to ease but not fall off a cliff,” Morgan Stanley strategists said.

They believe “that even as payrolls cool, a bumpy path ahead on inflation will keep the Fed from cutting before June, when we expect the first 25bp cut.”

Market participants should expect “fed funds futures to lower their odds of aggressive rate cuts in the first half of 2024,” BMO Economics’ Anderson said.

Fed Chairman Jerome Powell “will need to push back hard in his upcoming press conference on the rate-cut narrative that has taken hold in recent weeks,” he said.

NYC TFA touts successful sale of $1.4B of bonds

The New York City Transitional Finance Authority said Friday that its sale of $1.44 billion of future tax-secured subordinate bonds saw yields cut during

The deal was made up of about $1.27 billion of tax-exempt fixed-rate bonds and $173 million of taxables.

Proceeds will be used to refund certain outstanding bonds. The refunding achieves roughly $172 million in total debt service savings, the TFA said, spread evenly across fiscal years 2024 through 2027.

During the retail order period, the TFA received over $1.4 billion of orders with almost $2.7 billion of orders during the institutional pricing period, making the deal about 3.2 times oversubscribed.

Given institutional demand for the tax-exempts, yields were cut by two basis points in 2027, 2028 and 2030 through 2032; by three basis points in 2029, 2033 through 2035 and 2042; by five basis points in 2036 through 2039; and by seven basis points in 2040 and 2041. Final yields ranged from 2.63% to 3.93%.

TFA also competitively sold around $173 million of taxables that saw 10 bidders, with Morgan Stanley winning at a true interest cost of 4.748%.

Primary to come:

The City of Virginia Beach Development Authority (//BB+/) is set to price $463.4 million of Westminster-Canterbury on Chesapeake Bay residential care facility revenue bonds, consisting of $297.9 million Series A, $21 million of Series B-1, $41.5 million of Series B-2, $103 million of Series B-3. Ziegler.

Ohio (Aaa/AA+/AAA/) is set to price Tuesday $383.095 million of refunding general obligations bonds. Loop Capital Markets.

The San Bernardino Community College District (Aa1/AA//) is set to price Tuesday $221 million of general obligation bonds. Piper Sandler & Co.

The Greater Texoma Utility Authority, City of Sherman, Texas, (/AA//) is set to price $187.61 million of contract revenue bonds, serials 2027-2044, terms 2049, 2054, insured by Build America Mutual Assurance. Baird.

The Grand River Dam Authority (A1/AA-//) is set to price Tuesday $150 million of revenue bonds. Goldman Sachs & Co. LLC.

The New York City Housing Development Corp. is set to price Tuesday $148.615 million of multi-family housing revenue variable-rate sustainable development bonds, in two series, consisting of $32.615 million of refunding Series E-3 and $116 million of Series L-1 remarketing. Jefferies LLC.

Competitive:

Bridgewater-Raritan Regional School District, New Jersey, (Aa1///) is set to sell $150.658 million of school revenue bonds at 11 a.m. eastern Tuesday.

The Empire State Development Corp. is set to sell Thursday three series of personal income tax bonds, consisting of $344.02 million of PITs at 10:30 a.m. eastern, $249.805 million of climate bond certified PITs at 11:00 a.m. eastern and $252.805 million of climate bond certified PITs at 11:30 a.m. eastern.

Chip Barnett contributed to this story.