Municipals were mixed in secondary trading Tuesday amid an active primary that saw two large airport deals from Dallas-Fort Worth and Atlanta price. U.S. Treasuries were also mixed, and equities sold off.

The two-year muni-to-Treasury ratio Tuesday was at 63%, the three-year at 63%, the five-year at 63%, the 10-year at 65% and the 30-year at 86%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 63%, the 10-year at 65% and the 30-year at 86% at 4 p.m.

“While August is so far posting negative returns across fixed-income cohorts, municipal bonds are displaying outperformance, both on an absolute and tax-adjusted basis, thanks largely to constructive market technicals and the resiliency of overall demand for product against a summer backdrop of negative net supply,” said Jeff Lipton, managing director of credit research at Oppenheimer Inc.

The extended cycle of mutual fund outflows appears to “have been broken as the improved market tone has paved the way for intermittent weekly inflows,” he said.

He believes “a cyclical return to positive flows would require rate stability, further evidence of disinflation, and continued technical support.”

This outperformance has kept “tax-exempts more expensive relative to Treasury alternatives,” he said.

Due to “the tax-efficient and credit attributes along with the current yield benefits, investment in municipal securities helps to offset the impact of rate volatility and to maximize the potential for long-term total return,” he said.

With the 2018 income tax cuts sunsetting in 2025, Lipton said “the value of tax-exemption on munis can be expected to become more pronounced.”

In a near-perfect scenario, he noted “the economy slows without falling into recession and the Fed moves even closer to its 2% target, with perhaps something a bit higher offering an acceptable compromise.”

This would likely lead to a bull-steepening UST yield curve, but the said “there would have to be broader consensus that the tightening cycle has concluded.”

If this happens, munis may underperform “as an extended UST rally ensues, but if the supply/demand imbalance persists within the muni market, tax-exempts could break free from the Treasury market’s grip and follow its own performance trajectory,” according to Lipton.

“As reinvestment needs hold in with outperformance likely to promote richer valuations,” he said munis should continue to bid well.

However, as the summer comes to an end, he said “technicals can be expected to grow less supportive with munis finding it challenging to outperform taxable alternatives.”

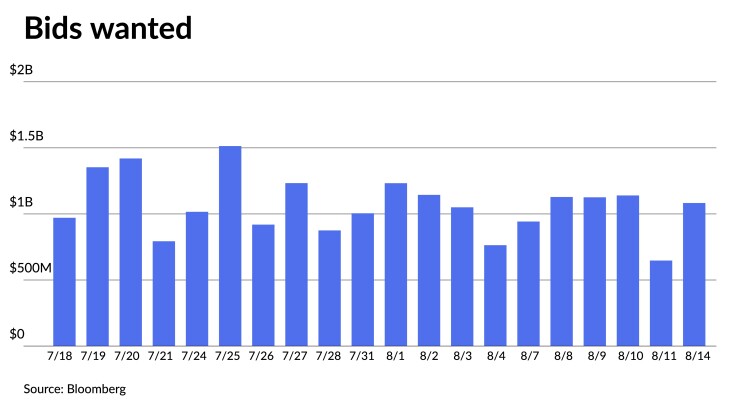

Summer redemption season ends Tuesday when issuers return $9 billion of matured or called bond principal, said CreditSights strategists Pat Luby and Sam Berzok.

Aug. 15 redemptions are heaviest in Texas at $4.9 billion, California at $1.2 billion and Pennsylvania at $643 million, they said.

From Wednesday through Aug. 31, they said only $3 billion will be returned, with $1.4 billion being paid out on the last day of the month. New York issuers, mostly New York City, will return $1.3 billion on Aug. 31, according to CreditSights strategists.

In September, they said “incremental demand from reinvestment flows will drop sharply as issuers will be paying out $19.6 billion, 56% less than will than will have been paid out in August.

Reinvestment flows for September are the second lowest of 2023, after April, they noted.

The Bond Buyer 30-day visible supply sits at $8.78 billion.

In the primary market Tuesday, BofA Securities priced for Atlanta (Aa3//AA-/AA+/) $706.900 million of airport revenue bonds. The first tranche, $206.565 million of non-AMT green airport general revenue bonds, Series 2023B-1, saw 5s of 7/2024 at 3.39%, 5s of 2028 at 3.02%, 5s of 2033 at 3.13%, 5s of 2038 at 3.61%, 5s of 2043 at 3.98%, 5s of 2048 at 4.15% and 5s of 2053 at 4.22%, callable 7/1/2033.

The second tranche, $27.375 million of non-AMT airport general revenue bonds, Series 2023B-2, saw 5s of 7/2024 at 3.39%, 5s of 2028 at 3.02%, 5s of 2033 at 3.13%, 4s of 2038 at 3.95%, 4.125s of 2043 at 4.31%, 4.25s of 2048 at 4.43% and 4.375s of 2053 at 4.52%, callable 7/1/2033.

The third tranche, $30.080 million of AMT airport general revenue bonds, Series 2023C, saw 5s of 7/2024 at 3.99%, 5s of 2028 at 3.69%, 5s of 2033 at 3.65%, 5s of 2038 at 4.15%, 5s of 2043 at 4.41%, 5s of 2048 at 4.52% and 5s of 2053 at 4.60%, callable 7/1/2033.

The fourth tranche, $38.960 million of non-AMT green airport passenger facility charge and subordinate lien general revenue bonds, Series 2023D, saw 5s of 7/2044 at 4.04%, callable 7/1/2033.

The fifth tranche, $256.225 million of AMT green airport passenger facility charge and subordinate lien general revenue bonds, Series 2023E, saw 5s of 7/2024 at 3.99%, 5s of 2030 at 3.61%, 5s of 2033 at 3.65%, 5s of 2038 at 4.10%, 5s of 2043 at 4.30% and 5.25s of 2048 at 4.37%, callable 7/1/2033.

The sixth tranche, $88.535 million of non-AMT airport general revenue refunding bonds, Series 2023F, saw 5s of 7/2025 at 3.40%, 5s of 2028 at 3.13% and 5s of 2033 at 3.21%, noncall.

The seventh tranche, $59.160 million of AMT airport general revenue refunding bonds, Series 2023G, saw 5s of 7/2025 at 3.98%, 5s of 2028 at 3.71% and 5s of 2030 at 3.66%, noncall.

Piper Sandler priced for the cities of Dallas and Fort Worth, Texas (A1/A+/A+/AA/), $691.305 million of Dallas Fort Worth International Airport joint revenue refunding and improvement bonds, Series 2023B, with 5s of 11/2024 at 3.53%, 5s of 2028 at 3.19%, 5s of 2033 at 3.41%, 5s of 2038 at 3.79%, 5s of 2042 at 4.05% and 5s of 2047 at 4.19%, callable 11/1/2033.

Goldman Sachs priced Colorado Springs, Colorado (Aa2/AA+//), $365.810 million of utilities system revenue bonds. The first tranche, $204.585 million of improvement bonds, Series 2023A, saw 3s of 11/2028 at 2.94%, 5s of 2033 at 3.05%, 5s of 2038 at 3.54%, 5s of 2043 at 3.87%, 5.25s of 2048 at 4.03% and 5/35s of 2053 at 4.11%, callable 11/15/2033.

The second tranche, $161.225 million of refunding bonds, Series 2023B, saw 5s of 11/2023 at 3.35%, 5s of 2028 at 2.94%, 5s of 2033 at 3.05%, 5s of 2038 at 3.54%, 5s of 2043 at 3.87% and 5.25s of 2045 at 3.93%, callable 11/15/2033.

Barclays priced for Idaho Housing and Finance Association (Aa1///) $149.375 million of fixed-rate non-AMT single-family mortgage bonds, 2023 Series C, with 5s of 1/2024 at 3.31%, 5s of 1/2028 at 3.49%, 5s of 7/2028 at 3.52%, 4s of 1/2033 at par, 4s of 7/2033 at par, 4.25s of 7/2038, 4.65s of 7/2043 at par, 4.75s of 7/2048 at par and 5.75s of 1/2053 at 4.25% and 4.8s of 7/2053 at par, callable 1/1/2033.

In the competitive market, Wisconsin (Aa1/AA+/AA+/AAA/) sold $271.360 million of GOs, Series 2023B, to Morgan Stanley, with 5s of 5/2025 at 3.22%, 5s of 2028 at 2.87%, 5s of 2033 at 2.85%, 5s of 2038 at 3.41%, 5s of 2043 at 3.68% and 5s of 2044 at 3.71%, callable 5/1/2032.

NYC TFA to sell $1B bonds

The New York City Transitional Finance Authority plans to issue $1 billion of future tax-secured subordinate bonds.

The tax-exempt fixed-rate bonds are expected to be priced Aug. 23, after investors will have priority in placing orders for the bonds during a one-day retail order period.

The bonds will be priced by book-running lead manager Wells Fargo Securities, with BofA Securities, Citigroup, J.P. Morgan, Jefferies, Loop Capital Markets, Ramirez & Co., RBC Capital Markets and Siebert Williams Shank as co-senior managers.

Proceeds will be used to fund capital projects. The TFA sold $1.08 billion of tax-exempt and taxable future tax-secured subordinate bonds in July.

Secondary trading

NYC 5s of 2024 at 3.25% versus 3.24% Monday and 3.27% Friday. Georgia 5s of 2025 at 3.13% versus 3.15% original on Friday. Washington 5s of 2026 at 3.04%-3.02%.

Wellesley, Massachusetts, 5s of 2028 at 2.65%. Virginia Public Building Authority 5s of 2029 at 2.82% versus 2.84% Monday. Nebo School District, Utah, 5s of 2030 at 2.79%.

NYC 5s of 2032 at 2.99%-3.01% versus 2.97% Friday and 3.00% original on Thursday. DASNY 5s of 2033 at 2.97%-3.00% versus 2.93% Thursday and 3.09% original on Aug. 3. California 5s of 2034 at 2.79%-2.81% versus 2.79%-2.75% Friday.

Harris County, Texas, 5s of 2048 at 4.09%-4.08% versus 4.06%-4.01% original on Aug. 9. Clark County Water Reclamation District, Nevada, 5s of 2049 at 4.02% versus 4.00% Thursday. NYC 5s of 2051 at 4.22%-4.20% versus 4.18%-4.16% Friday and 4.20%-4.15% original on Thursday.

AAA scales

Refinitiv MMD’s scale saw cuts outside of five years: The one-year was at 3.22% (-2) and 3.10% (unch) in two years. The five-year was at 2.77% (unch), the 10-year at 2.75% (+5) and the 30-year at 3.71% (+2) at 3 p.m.

The ICE AAA yield curve saw cuts throughout most of the curve: 3.25% (-2) in 2024 and 3.14% (unch) in 2025. The five-year was at 2.77% (+1), the 10-year was at 2.71% (+2) and the 30-year was at 3.71% (+2) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut outside of five years: 3.23% (-2) in 2024 and 3.10% (unch) in 2025. The five-year was at 2.78% (unch), the 10-year was at 2.76% (+4) and the 30-year yield was at 3.70% (+2), according to a 4 p.m. read.

Bloomberg BVAL was cut one to four basis points: 3.19% (+1) in 2024 and 3.09% (+1) in 2025. The five-year at 2.77% (+2), the 10-year at 2.73% (+4) and the 30-year at 3.71% (+2) at 4 p.m.

Treasuries were mixed.

The two-year UST was yielding 4.938% (-3), the three-year was at 4.636% (-1), the five-year at 4.364% (flat), the 10-year at 4.212% (+2), the 20-year at 4.500% (+2) and the 30-year Treasury was yielding 4.321% (+3) at the close.

Primary to come

Dallas and Fort Worth are also set to price Wednesday $239.725 million of alternative minimum tax Dallas Fort Worth International Airport joint revenue refunding bonds, Series 2023C, serials 2024-2033. Cabrera Capital Markets.

The Regents of the University of California (Aa2/AA/AA/) is set to price Wednesday $608.160 million of general revenue bonds, Series 2023BQ, serials 2029, 2031, 2033, 2035. Siebert Williams Shank & Co.

The Regents of the University of California is also set to price Wednesday $120.045 million of taxable general revenue bonds, Series 2023BR, serial 2033. Siebert Williams Shank & Co.

The Los Angeles Unified School District (A2//A-/) is set to price Thursday $384.260 million of certificates of participation, sustainability bonds, Series 2023A, serials 2024-2038. BofA Securities.

The Dormitory Authority of the State of New York (Aa2//AA/) is set to price Thursday $300 million of New York and Presbyterian Hospital Obligated Group revenue bonds, Series 2023A. Goldman Sachs.

Chicago (/AA//) is set to price Wednesday $181.295 million of Build America Mutual-insured Chicago O’Hare International Airport customer facility charge senior lien refunding bonds, Series 2023, serials 2028-2043. Barclays.

The Colorado Housing and Finance Authority (Aaa/AAA//) is set to price Wednesday $180 million of federally taxable single-family mortgage class-I bonds, Series 2023 N-1, serials 2026-2033, terms 2038, 2041, 2053. RBC Capital Markets.

Competitive:

Tennessee (Aaa/AAA/AAA/) is set to sell $499.420 million of GOs, Series 2023A, at 10:15 a.m. Wednesday and $44.745 million of federally taxable GOs, Series 2023B, at 10:45 a.m. Wednesday.